Resources

Our relationship with you is built on trust and transparency. With an aim of keeping you thoroughly informed, we offer valuable information about our funds and more, below. Access our fact sheets, prospectuses, performance reports, and materials for use with clients.

Rules-Based Process in Motion Snapshot: Tactical Risk Spectrum 50 Fund Ending June 30, 2025

Reflects how our truly tactical rules-based investment process reacted due to market movement through June 30, 2025.

View Resource

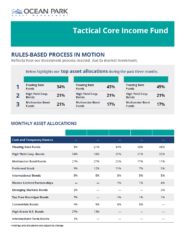

Rules-Based Process in Motion Snapshot: Tactical Core Income Fund Ending June 30, 2025

Reflects how our truly tactical rules-based investment process reacted due to market movement through June 30, 2025.

View Resource

Rules-Based Investment Process in Motion Synopsis: Active ETFs Through June 30, 2025

Reflects how our truly tactical, rules-based investment process reacted with regard to the Ocean Park Active ETFs due to market movement through June 30, 2025.

View Resource

Rules-Based Investment Process in Motion Synopsis: Mutual Funds Through June 30, 2025

Reflects how our truly tactical, rules-based investment process reacted with regard to the Ocean Park Mutual Funds due to market movement over the past 18 months up through June 30, 2025.

View Resource

Rules-Based Investment Process in Motion Synopsis: Ocean Park Models Through June 30, 2025

Reflects how our truly tactical, rules-based investment process reacted with regard to the Ocean Park Models due to market movement over the past 18 months up through June 30, 2025.

View Resource

Rules-Based Investment Process in Motion Synopsis: Strategies Through June 30, 2025

Reflects how our truly tactical, rules-based investment process reacted with regard to the Ocean Park Strategies due to market movement over the past 18 months up through June 30, 2025.

View Resource

Rules-Based Process in Motion Snapshot: Conservative Allocation Strategy Ending June 30, 2025

Reflects how our truly tactical rules-based investment process reacted due to market movement through June 30, 2025.

View Resource

Rules-Based Process in Motion Snapshot: Moderate Allocation Strategy Ending June 30, 2025

Reflects how our truly tactical rules-based investment process reacted due to market movement through June 30, 2025.

View Resource

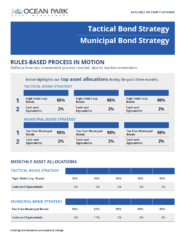

Rules-Based Process in Motion Snapshot: Tactical Bond Strategy & Municipal Bond Strategy Ending June 30, 2025

Reflects how our tactical rules-based investment process reacted due to market movement through June 30, 2025.

View Resource

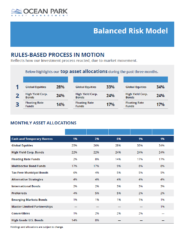

Rules-Based Process in Motion Snapshot: Balanced Risk Model Ending June 30, 2025

Reflects how our truly tactical rules-based investment process reacted due to market movement through June 30, 2025.

View Resource

Rules-Based Process in Motion Snapshot: Strategic Income Strategy Ending June 30, 2025

Reflects how our truly tactical rules-based investment process reacted due to market movement through June 30, 2025.

View Resource

Tactical Core Income Fund Performance vs. Fixed Income Sectors Ending March 31, 2025

A visual view of the Ocean Park Tactical Core Income Fund performance against fixed income sectors from 2012 to 2024.

View Resource

Ocean Park Tactical Bond Fund: Performance Snapshot through June 30, 2025

Monthly performance analysis booklet for the Ocean Park Tactical Bond Fund sourced through Morningstar, updated through June 30, 2025.

View Resource

Ocean Park Tactical Core Income Fund: Performance Snapshot through June 30, 2025

Monthly performance analysis booklet for Ocean Park Tactical Core Income Fund sourced through Morningstar. Updated through June 30, 2025.

View Resource

Ocean Park Tactical Municipal Fund: Performance Snapshot through June 30, 2025

Monthly performance analysis booklet for the Ocean Park Tactical Municipal Fund sourced through Morningstar, updated through June 30, 2025.

View Resource

Ocean Park Mutual Funds: Trailing Returns Performance Snapshot through June 30, 2025

Monthly performance analysis booklet for the Ocean Park Mutual Funds, updated through June 30, 2025.

View Resource

Performance Snapshot: Global Balanced Series Through May 31, 2025

Performance analysis for Ocean Park Global Balanced Series, approved for client use, and updated through May 31, 2025.

View Resource

Performance Snapshot: SMA Programs Through May 31, 2025

Performance analysis for Ocean Park Programs, approved for client use, and updated through May 31, 2025.

View Resource

Performance Snapshot: Models Through May 31, 2025

Performance analysis for Ocean Park Models, approved for client use, and updated through May 31, 2025.

View Resource

Performance Snapshot: Strategies Through May 31, 2025

Performance analysis for a select number of Ocean Park Strategies, approved for client use, and updated through May 31, 2025.

View Resource

Ocean Park Active ETFs: Performance Snapshot through June 30, 2025

Performance analysis for Ocean Park Active ETFs, approved for client use, and updated through June 30, 2025.

View Resource

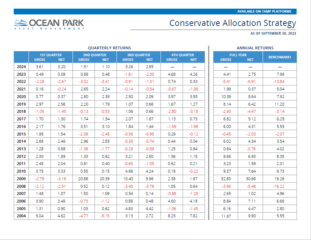

Conservative Allocation Strategy - Quarterly Returns vs. Annual Returns

Conservative Allocation Strategy - Quarterly Returns vs. Annual Returns (Q1 2025)

View Resource

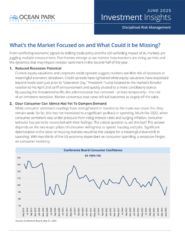

What the Market is Focusing on and What it Could Be Missing

Ocean Park’s June 2025 Investment Insights highlights five key market themes, including reduced recession fears, resilient consumer spending, mixed labor signals, the disruptive impact of AI, and uncertainty around trade policy and Fed flexibility.

View Resource

Looking Beyond the Agg

Explore how Ocean Park’s fixed income strategies go beyond the Bloomberg US Aggregate Bond Index to uncover broader opportunities and enhance portfolio diversification.

View Resource

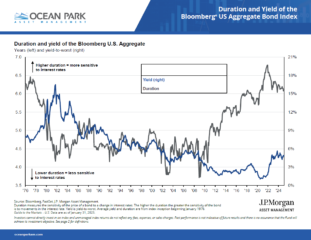

Duration and Yield of the Bloomberg U.S. Aggregate Bond Index

This flyer shows the duration and yield of the Bloomberg U.S. Aggregate Bond Index from January 1, 1976 through March 31, 2025.

View Resource

Municipal Bonds are Anything but Boring

Municipal bonds are supposed to be boring, but we believe they’ve been anything but boring. The environment has created an opportunity for tax harvesting and for evaluating how you allocate to municipal bonds.

View Resource

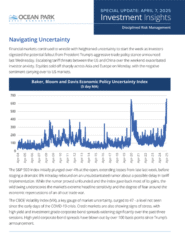

Navigating Uncertainty

Special Update of Investment Insights: Chief Investment Officer, provides perspective on the evolving volatility of the global equity market.

View Resource

Tariff Tumult: Global Markets Tumble as Trump Imposes Sweeping Import Tariffs

Chief Investment Officer James St. Aubin speaks on the effects of President Trump's "Liberation Day" tariffs.

View Resource

Death of an Expansion Cycle

Investments take the escalator up, and the elevator down.

View Resource

Too Much of a Good Thing? Examining the Risks of America’s Growing National Debt

Chief Investment Officer James St. Aubin examines the risks of America’s growing national debt.

View Resource

Bull & Bear Markets – Strategic Income Strategy Analysis

See how Ocean Park’s Strategic Income Strategy performed in bull and bear bond markets.

View Resource

Bull & Bear Markets – Tactical Core Income Fund Analysis

See how Ocean Park’s Tactical Core Income Fund performed in bull and bear bond markets.

View Resource

Riding High, Looking Ahead: Markets at a Crossroads

Chief Investment Officer James St. Aubin reviews 2024 and shares relevant data regarding the 2025 economic and market outlook.

View Resource

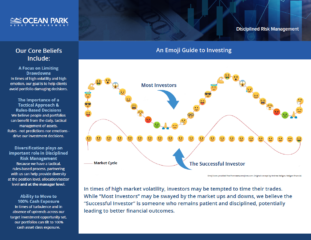

Emotions of Investing

While “Most Investors” may be swayed by the market ups and downs, we believe the “Successful Investor” is someone who remains patient and disciplined, potentially leading to better financial outcomes.

View Resource

Efficiently Designed Global Portfolios, To Keep You Well Invested

Ocean Park's Global Balanced Portfolios Series brochure.

View Resource

Navigating Our Solutions

An all-in-one brochure that covers our core beliefs, investment process, funds, and strategies.

View Resource

Moderate Allocation Strategy Brochure

The Moderate Allocation Strategy seeks to enhance return with increased global stock exposure while providing investors integrated risk management disciplines.

View Resource

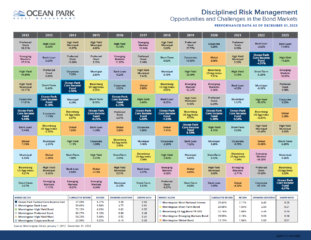

Our Investment Process

Learn about Ocean Park Asset Management’s disciplined risk management approach and investment process.

View Resource

Firm Overview

An overview of our firm, philosophy, investment process, solutions, and investment team.

View Resource

Performance During Two Major Downturns: Ocean Park Conservative Allocation Strategy

A look at the Ocean Park Conservative Allocation Strategy during the 2008 financial crisis and major market sell-offs.

View Resource

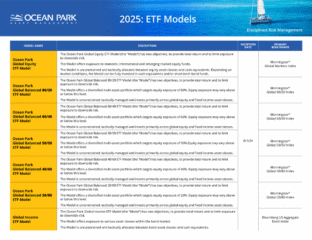

ETF Models Profile Page

Ocean Park ETF Models have two objectives, to provide total return and to limit exposure to downside risk.

View Resource

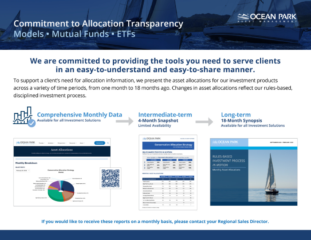

Our Commitment to Allocation Transparency

We are committed to providing you with tools that make your life easier as an advisor. Among the many ways we achieve this are through the variety of asset allocation reports that we make available.

View Resource

Tactical Bond Strategy Brochure

An alternative approach to a traditional asset class.

View Resource

Risk-on vs. Risk-off: Tactical Bond Strategy

See risk-on and risk-off investments since the strategy's inception, as well as the percentage allocated to cash, January 2022 - December 2023.

View Resource

2024 Capital Gains Distribution Estimates

View Resource

Ocean Park ETF Profile

View Resource

Beneficiary Individual Retirement Account (IRA) Custodial Agreement and Disclosure Statement

View Resource

Beneficiary ROTH Individual Retirement Account (IRA) Custodial Agreement & Disclosure Statement

View Resource

Coverdell Education Savings Account (ESA) Application

View Resource

Coverdell Education Savings Account (ESA) Custodial Agreement and Disclosure Statement

View Resource

Form ADV Part 2A

View Resource

Form ADV Part 2B

View Resource

Form CRS

View Resource

Individual Retirement Account (IRA) Custodial Account Adoption Agreement

View Resource

Individual Retirement Account (IRA) Custodial Account Agreement and Disclosure Statement

View Resource

Individual Retirement Account (IRA) Transfer of Assets Form

View Resource

Investor Privacy Policy

View Resource

Mutual Fund Account Application & Privacy Notice

View Resource

Non-Qualified Transfer of Assets Form

View Resource

ROTH Individual Retirement Account (IRA) Custodial Agreement and Disclosure Statement

View Resource

SIMPLE Individual Retirement Account (IRA) Custodial Account Adoption Agreement Application

View Resource

SIMPLE Individual Retirement Account (IRA) Custodial Account Agreement and Disclosure Statement

View Resource

Wrap Fee Program Brochure

View Resource

The Core Fixed Income Challenge: Muting the Sounds of Intellectual Noise

Why fixed income market calls—especially since 2022—have proven to be unreliable, and what potential strategies and solutions advisors may have.

Log In/Create Account

NASDAQ Just for Funds: Managing Risk in Volatile Markets

James St. Aubin, CIO at Ocean Park Asset Management, joined Nasdaq’s Just for Funds to discuss the firm’s distinctive risk-managed investment approach.

View Resource

Quarterly Webcast Q1 2025

CIO James St. Aubin unpacks key Q1 2025 market trends, while our chief strategist shows how Ocean Park adapted with rules-based strategies.

Log In/Create Account

FintechTV: Markets see back and forth trading in April amid tariff uncertainty

James St. Aubin, CIO & Portfolio Manager at Ocean Park Asset Management, joins Remy Blaire to take us through the rollercoaster S&P 500 price action and what it says about market sentiment.

View Resource

CIO Insights Special Update: April 8, 2025

James St. Aubin discusses recent financial market volatility triggered by President Trump's hawkish tariff announcement.

View Resource

TAMPs: The Value of Outsourcing

Director of National Accounts, Tiana Brenneise, speaks about the value of outsourcing.

View Resource

NASDAQ Just for Funds: Navigating Market Risks with Ocean Park’s New ETFs

Danielle Retsky from Nasdaq interviews James St. Aubin, the Chief Investment Officer of Ocean Park Asset Management.

View Resource

CIO Insights: June 14, 2024

In June’s CIO Insights, James St. Aubin unpacks recent economic reports and the Fed’s June meeting in relation to the markets.

View Resource

About Us

Since 1989, our founders' rules-based, buy-and-sell disciplines have sought to help investors limit downside risk, grow their wealth, and achieve their investment goals.

View Resource

The Founders' Series, Episode 1 | The Founders

View Resource

The Founders' Series, Episode 2 | A Meeting Of Minds

View Resource

The Founders' Series, Episode 3 | Two Floppy Drives And a Westie

View Resource